UNITY BANK RECONSTRUCTION PROPOSAL, A WELL THOUGHT OUT PLAN

YET WITH A BUT!!!

After reading the news about UNITY

BANK intention to do a share reconstruction process, I personally felt it’s a

welcome idea which is even long overdue.

The banks in the banking sector of the Nigeria capital

market has a characteristic feature which lies in their over-bloated outstanding

shares. Considering the first ten companies with the highest outstanding share

in the Nigeria stock exchange shows the banks occupying seven out of the ten

slots.

SN

|

COMPANY

|

OUTSTANDING SHARES(MILL)

|

1

|

Transcorp

|

38720

|

2

|

UnityBank

|

38446

|

3

|

UBA

|

32981

|

4

|

FirstBank

|

32632

|

5

|

ZenithBank

|

31936

|

6

|

GTBank

|

29431

|

7

|

FidelityBank

|

28974

|

8

|

AccessBank

|

22882

|

9

|

Afrinsure

|

20585

|

10

|

Roads

|

20000

|

Focusing on the banks alone also

shows Unity Bank with the highest outstanding shares in the entire banking

sector.

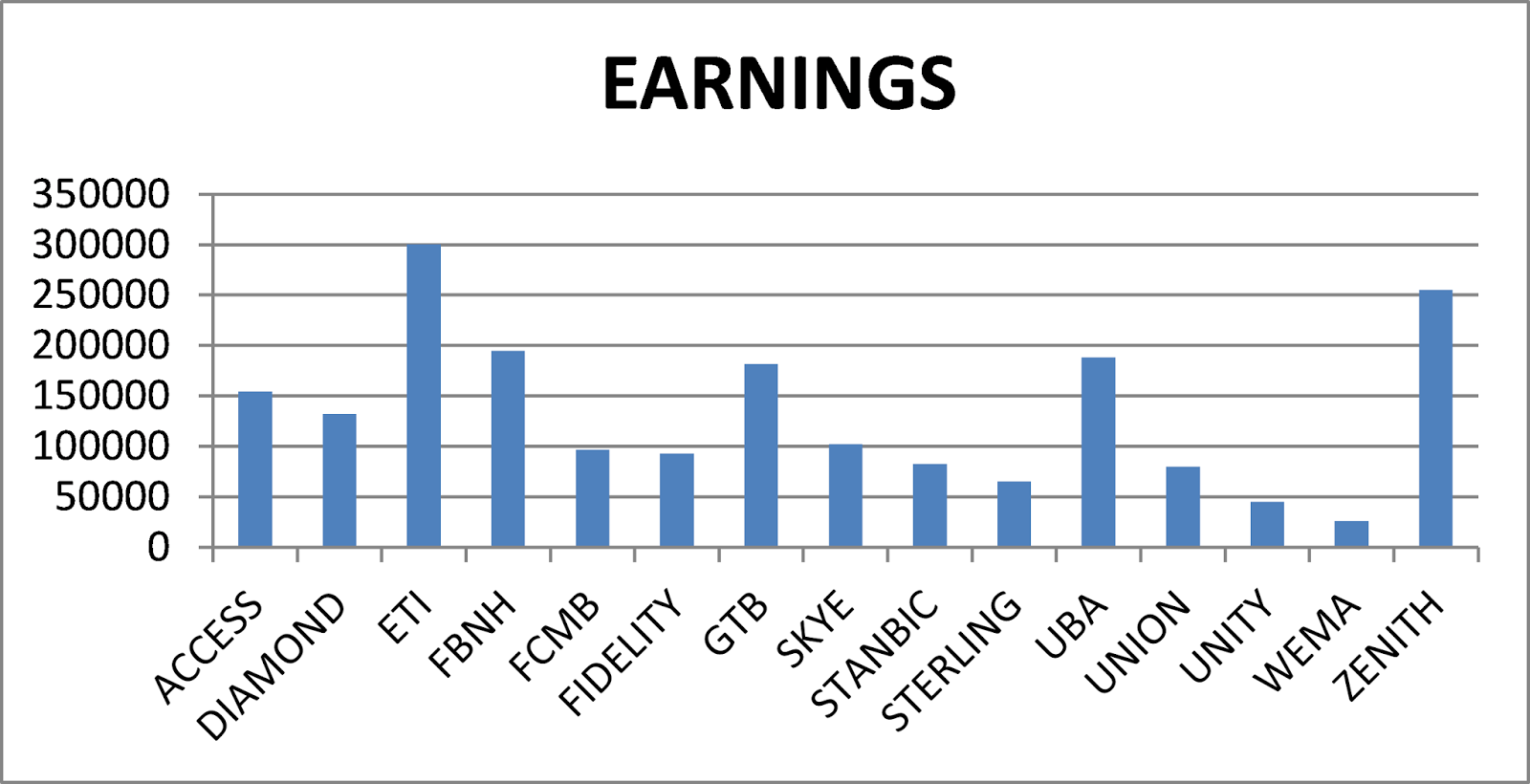

The most intriguing fact about

UNITY BANK is that while banks with lower OS in comparison to

Unity Bank are generating higher Earnings and PAT to mitigate whatever negative

effect that might arise from their blossom outstanding shares, Unity bank is

not. The graph below show Nigerian banks as they stand according to their 3rd

quarter results.

NB- FBNH 2nd quarter result was used here.

It therefore makes it imperative to note that no other bank needs a share reconstruction than Unity Bank. What will be the benefits

of a share reconstruction to this bank?

REDUCED OUTSTANDING SHARES

REDUCED OUTSTANDING SHARES

Should the reconstruction

be carried out, the outstanding share of Unity bank will drastically reduce

from the current 38446mil to 9612mill automatically making it the bank with the

lowest outstanding shares in the banking sector of the Nigeria stock exchange.

INCREASE

IN EPS VALUE

Apart from the

above, should Unity bank successfully reconstructs it shares, the action will

project its earnings per share (EPS) from the current meager EPS value.

CHANGE IN QUOTED PRICE

Unity bank as at

24/12/13 is selling at .50k should there be a successful share reconstruction

in the future this will change the current price to N2.00

·

PRE-RECONSTRUCTION

|

POST-RECONSTRUCTION

|

|||||||

OS

|

Q3/13 EARNINGS

|

Q3/13 PAT

|

CURRENT PRICE

|

QE/13 EPS

|

OS

|

Q3/13 EPS

|

PROSPECTIVE PRICE

|

|

UNITY

|

38446Mill

|

45395mill

|

1153Mill

|

.50k

|

0.03k

|

9611mill

|

0.12k

|

N2.00

|

What could however be the possible pitfalls

in UNITY BANK potential re-construction process?

o QUOTED PRICE FALLING POST-RECONSTRUCTION

Without trying to

be a prophet of doom, I have this sympathetic feeling that Shareholders of

unity bank will be the end loser in this reconstruction proposal, am afraid

because I have been asking myself if UNITY bank has what it takes to go beyond

N2 in the short and medium term should the bank successfully reconstruct its shares,

to be more candid, does Unity bank has what it takes in terms of current

earnings to stay at N2.00 without plummeting back to pre-construction price?

o

INTENTION

TO RAISE MORE CAPITAL

No doubt about Unity Bank dire need to shore up its capital in order to compete effectively in the

industry but raising authorized share capital, reconstructing of shares and at

the same time trying to raise more capital makes the entire process a questionable

flip-flop which I think shareholders will be the end loser of the game plan. it is

thus disturbing that it is the same shareholders gave their approval to all of

the above in UNITY BANK recent EGM recently held in Lagos. The entire scenario gives me

no choice than to wish Unity Bank and its shareholder best of luck in the

prospective effort to make Unity Bank a bank to reckon with in the banking

industry.

Questions, advice and Comments will

be positively received.

Follow me on twitter - @1himself